Capitalisation of product development costs means carrying forward the cost effect of product development costs incurred to future accounting periods. For example, a software company develops a new version of its software product. It comes out during the accounting period that is expected to generate revenue over the next five years. The software enterprise may capitalise the product development costs incurred during the period. They can also amortise the capitalised development costs over the next five years.

Start-ups are characterised by strong investments in product development. In the first years of operation, the business is usually loss-making. This is due to as there is often no income yet or costs exceed income. By capitalising product development costs on the balance sheet, the cost effect of product development expenditure is deferred. So then that the costs are not a burden on the company’s results until the corresponding revenues are generated. In practice, start-ups are often forced to do this because the sufficiency of the company’s equity becomes critical. See example below.

You can also watch a related video where the examples are clearly explained.

What is development?

- Design of tools, patterns, moulds, etc. requiring new technologies

- Design, construction and testing of prototypes and models

- Development of new software products and substantial improvement of existing ones, where the aim is to develop computer technology

- Design, construction and operation of the pilot plant until it becomes a production unit

According to the Accounting Act, development costs must be amortised over their useful life, but not more than ten years. The key to meeting capitalisation requirements is to estimate future revenue. For example, by estimating how much turnover/sales margin the product/service under development will generate during the period of impact. Sometimes it is difficult to set a depreciation period because forecasting the future is challenging. Typical amortisation periods for Valjas’ customers are usually 3-5 years, especially for software technology development projects.

What expenditure can be capitalised as development expenditure?

- Direct expenditure on development activities, including salaries and incidental expenses of persons directly involved in the activities

- Interest expenditure on development activities

Development costs may be capitalised if they are expected to generate income over several financial years. It is highly recommended that development expenditure be tracked in the accounts, for example by cost centre, so that development expenditure to be capitalised can be easily identified. Capitalised product development costs are depreciated annually in accordance with the depreciation plan.

Accordingly, research costs may not be capitalised on the basis of KPL 5:8§, but are treated as an annual expense in the company’s accounts. Research activities include, for example, the search for, evaluation and selection of objects for development activities. The Accounting Act deals with the amortisation of research and development costs in chapter 5:8.

A development project may also give rise to other intangible rights, for example in the form of a patent. Patents are capitalised as a separate item in the balance sheet.

Why should development costs be capitalised on the balance sheet?

The capitalisation of product development costs improves the result for the financial year. Financial statements can be thought of as a business card for a company. This is often important on how the company’s key figures look in the financial statements. The company’s stakeholders will judge the company on the basis of the financial statements. This happens, for example, when a bank grants financing. If investments in product development have been made during the financial year and the result for the financial year looks weak or even loss-making, it is worth considering capitalising the costs of product development. By capitalising product development costs, the result for the financial year is improved and the cost of the expenditure is carried over over several years.

For more mature start-ups, one form of funding is often Business Finland’s product development loans. The use of loan money puts a strain on the company’s equity and self-sufficiency, but by activating development expenditure, the situation can be improved.

At the beginning of a loan-financed project, the company’s management should assess the company’s balance sheet. The Valjas team can, for example, help by preparing a financial forecast for your company.

What is the impact of capitalising product development expenditure on a company’s figures?

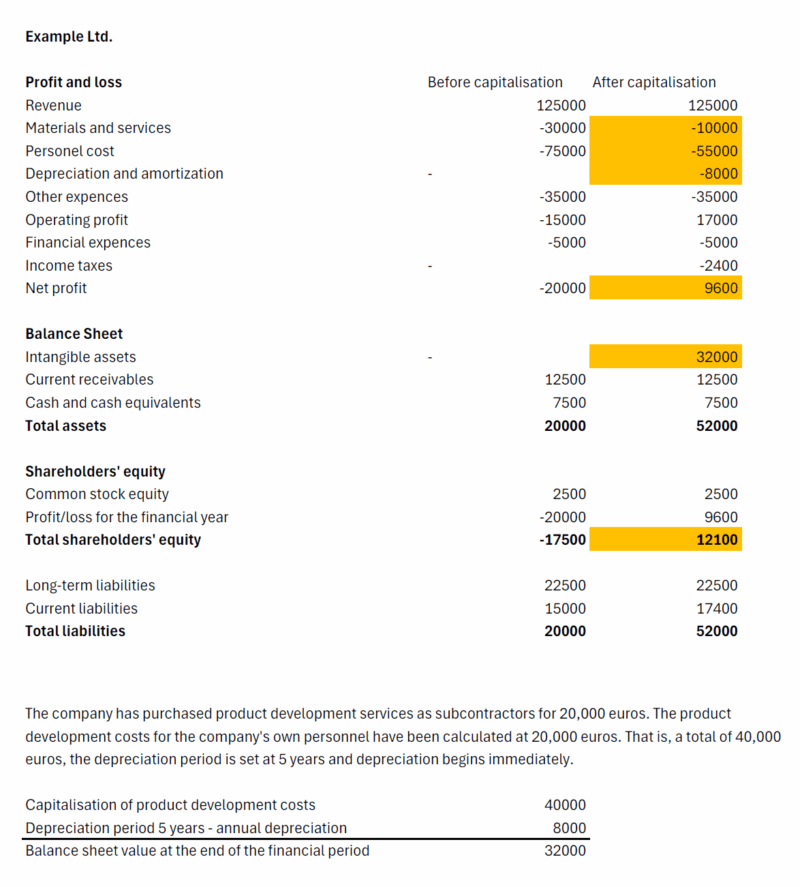

The first financial year of the example company has ended. The year ended and the company has a negative result of EUR 20 000. The company’s equity is also negative, which would lead to the loss of equity having to be registered with the Trade Register. Fortunately, however, the situation is not so negative.

The company has subcontracted product development for EUR 20 000 (VAT 0%) and the company’s own staff wage costs for development activities amount to EUR 20 000. These costs are capitalised in the balance sheet as development costs. The company estimates the useful life of the development costs to be 5 years and the depreciation period is set accordingly. Depreciation will start immediately from the current financial year.

Example

In the figure below you can see how the capitalisation of product development expenditure affects the company’s figures. Subcontracted services and personnel costs are adjusted out of these items in the profit and loss account and capitalised in the balance sheet. In addition, depreciation of capitalised product development costs is recorded at EUR 40 000 / 5 years = EUR 8 000 per year. The capitalised development costs are entered in the assets side of the balance sheet under intangible assets. Development costs from previous years can no longer be capitalised as they have to be booked on an accrual basis.

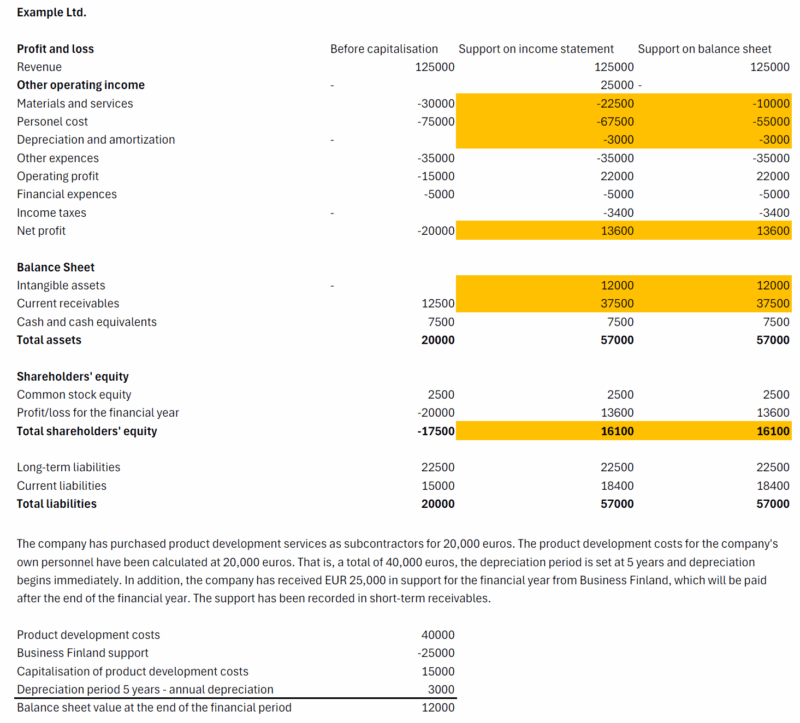

Attention! If the company has received support from Business Finland for product development costs, the share of the support for development costs must be deducted from the amount to be capitalised. Alternatively, support from Business Finland can be entered in the balance sheet as a deduction from capitalisable product development expenditure. Both options are described in the example below. The end result in terms of numbers is the same, only the presentation is different.

Please note that the project costs reported to Business Finland may not be exactly the same as the costs that can be capitalised. Business Finland’s project may not necessarily be allowed some costs that are eligible for capitalisation and vice versa.

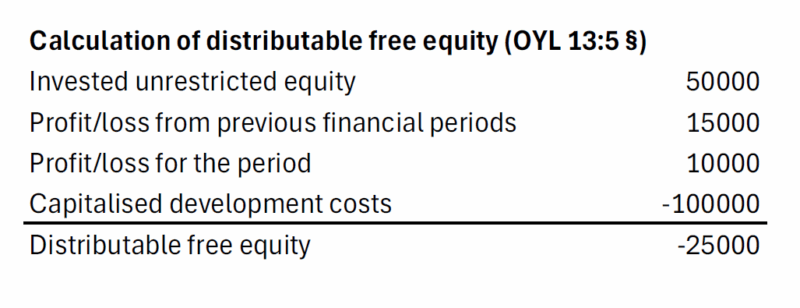

Impact of development expenditure on the company’s distributable assets

Under the new accounting law that came into force in 2016, capitalised development costs reduce the company’s distributable assets. Below is an example of a company with positive equity but no distributable free equity due to capitalised development costs. In other words, the company cannot pay a dividend.

Documentation of development expenditure

As mentioned above, it is highly recommended to distinguish development expenditure in the accounts, for example by cost centre, where the expenditure can be fully traced. Of course, it is also possible to collect the costs, for example in an excel workbook, and add it to the accounting records as an annex to the entry. For example, which purchase invoices have been capitalised and which person’s salary costs for which period have been capitalised.

In addition, it is highly recommended to document in a list what expenses have been capitalised and how much they are expected to generate income over their useful life.

How can Valjas help your business?

At Valjas, we help startups build a strong financial foundation from day one. Our team understands the unique challenges of early-stage growth. We know the cycle all the way from managing Business Finland projects to funding reports to keeping accounting, compliant, and future-proof. We guide you through financial planning, cost tracking, and reporting so you can focus on scaling your business with confidence. With Valjas as your accounting partner, you gain more than bookkeeping — you gain a team that understands innovation, growth, and the numbers behind success.

Please contact us. Let’s look at the right package for your business!