Value added tax (VAT) is the consumption tax that the seller of a good or service adds to the selling price. VAT is collected by the seller from the buyer each time the goods or services are sold and paid to the government.

In principle, a VAT-registered business can deduct the VAT included in the purchase price of the goods and services it buys when the goods are acquired for a taxable business activity. Thus, the VAT is ultimately paid by the consumer, as businesses in the service or production chain are allowed to deduct VAT on their purchases.

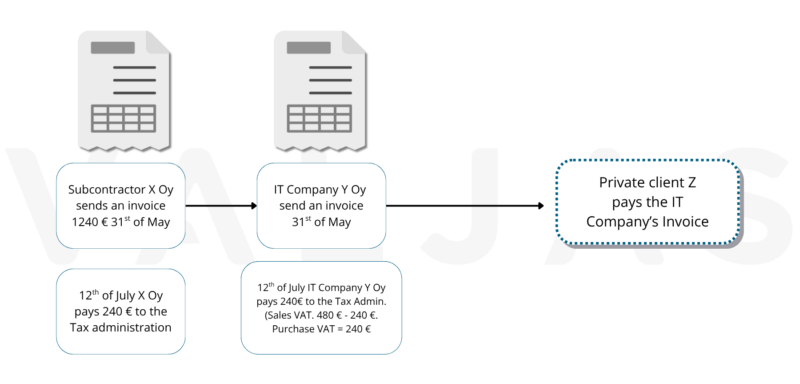

VAT – Example

For example, Subcontractor X Oy sells software development services to IT Yhtiö Oy for EUR 1000 + VAT 25,5%. The total amount of X Oy’s invoice is EUR 1255. Both companies are engaged in VAT-registered activities and are entitled to deduct VAT on their purchases.

That is, IT Company Ltd is allowed to deduct the VAT of 255 euros included in Subcontractor X’s invoice. IT Company Ltd resells its own service for €2000 + VAT 25,5% to private customer Y, so the total invoice amount is €2510. The tax is therefore not recurring in this case in a business-to-business transaction as it is deductible.Private customer Y is not entitled to deduct VAT, so his total cost is €2510.

VAT derogations and rates

VAT is added to invoices, regardless of whether the buyer is a business or a consumer. An exception to this rule is reverse charge VAT in the construction sector. The VAT liability of the buying company also has no bearing on whether VAT is added to the sales invoice. VAT on foreign trade is a case-by-case matter and a knowledgeable accountancy partner will be happy to help with VAT on foreign trade.

A business that is subject to VAT must register for VAT. An exception is made for small businesses where the turnover for the financial year (12 months) is less than €20 000. However, even if the turnover is below this threshold, the business can still register for VAT. This will be discussed in more detail in subsequent articles.

Tax rates on goods and services*:

- 25,5% general rate: most goods and services

- 14% reduced rate: food, feed, restaurant and catering services,books, medicines, sports services, cinema screenings, admission to cultural and entertainment events, passenger transport, accommodation services

- 10% reduced rate: magazines and newspapers

*) in 2025

Activities excluded from VAT include.

- Sale and rental of real estate and condominiums

- Health and medical care and social work

- Educational services specifically defined in the VAT Act

- Financial and insurance services

- Compensation for copyright and performances as defined in the VAT Act

- Universal postal services

For more information on VAT, see the Tax Administration’s website.