Start-up entrepreneurs, check at least these things before the accountant closes the books for the financial year! Even if you don’t understand anything about financial statements, this list will help you go through them with your accountant.

Too many times we have found, in retrospect, that these issues have not been addressed in previous financial years. Sometimes they have resulted in serious problems in later financial years.

Capital adequacy

Is equity in danger of falling into the deep freeze? Typically, a start-up company makes a loss for several years, even in the early stages of its operations. Almost every start-up struggles with the sufficiency of equity capital. The equity situation should be examined well in advance of the financial statements. In other words, a few months before the end of the financial year.

In addition, it is a good idea to look at the estimated loss for the rest of the financial year. This will help to predict the amount of equity at the balance sheet date. After the end of the financial year, the options for corrective action are limited. It is also worth looking at the next financial year – will there be enough equity to what extent?

Negative equity has a negative impact on a company’s credit rating. In practice, it can also be a barrier to obtaining finance. The loss of equity capital must be registered with the Patent and Registration Office.

Below are some options for correcting equity.

Development expenditure

Typically, start-ups organise a funding round to raise capital to cover early stage losses. In addition to equity funding, a product development loan may be available from Business Finland. A product development loan often poses challenges in terms of equity sufficiency. There is often a practical need to capitalise development expenditure. Development expenditure must have an expectation of future returns; if it does not, it cannot be capitalised.

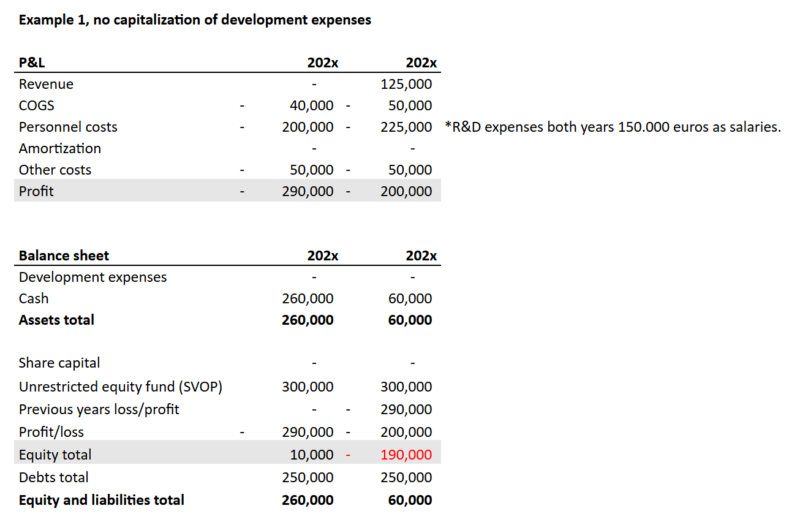

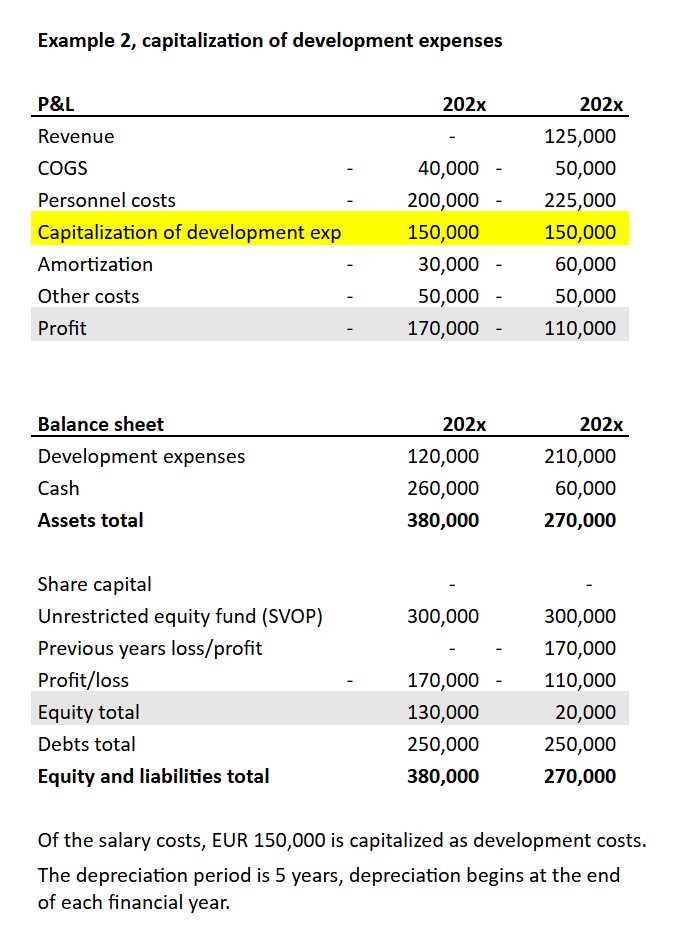

Let’s look at an example: a company receives €300 000 in equity financing (share issue). In addition, Business Finland will provide a €250 000 product development loan. Below you will find examples of equity without capitalisation of development costs and when development costs are capitalised. In the first example, the equity is almost completely eaten up in the first financial year. In the second financial year, the equity goes into the deep freeze.

In example two, the equity will last until the end of the second financial year. However, the sufficiency of equity will certainly be a challenge in the financial year 202x, unless the company turns profitable.

Attention! Example 2 assumes that the enterprise has incurred eligible costs that can be capitalised as development costs. The capitalisation of development expenditure is therefore not an automatic operation that can be carried out in all situations. Rather than being over-optimistic, be cautious when capitalising development expenditure.

Development expenditure previously capitalised

Previously activated development expenditure should also be reviewed. Sometimes it happens that a company decides to pivot in a completely different direction because the previously chosen business model is not successful in the market. If the company has capitalised development expenditure from such activities and is running down the entire business, the development expenditure should also be written down once. If, for example, part of the previous development work can be used in the new business, no write-down is necessary in this respect. A one-off write-down may pose challenges to the adequacy of equity. However, write-downs should not be postponed but should be made.

Capital loan

Capital loans can be both debt and equity. Debt is the most common type. In this case, the subordinated loan is shown as a separate item in the balance sheet after equity. If equity is negative, but the amount of the capital loan granted to the company exceeds the amount of negative equity, equity is considered to be covered.

In this case, the following item is added to the notes to the financial statements;

In addition, it is possible to provide equity-linked subordinated loans. In this case, the loan may not have a maturity date. In general, not many entities are willing to provide such a loan because there is no maturity date for repayment. It is therefore entirely up to the board of directors of the company at what point the equity loan is repaid, if at all.

So-called ordinary debt to a company can also be converted into a subordinated loan. For example, the owners of a company have lent the company EUR 50 000 in 2020. At the balance sheet date, equity is found to be negative by EUR 30 000. The loss of equity can be avoided by converting the loans from the owners into a subordinated loan or into a reserve for invested free equity (SVOP).

Investing in the SVOP fund

If there are challenges with the sufficiency of equity, additional capital can be raised from the owners of the company. If all shareholders are willing to invest in proportion to their shareholdings, the investment can be made directly into the SVOP fund without a separate share issue.

This is a very light administrative procedure. However, it is often necessary to resort to a share issue because only some of the shareholders are prepared to finance the company or have the necessary financial resources.

Share issue

In start-ups, a share issue is usually tantamount to a funding round. In other words, new shares in the company are issued in exchange for investment, i.e. it would be a paid share issue. It is almost always a directed issue, whereby the issue is directed to specific parties. In this case, the shares are subscribed only by these specific parties. A directed share issue must always have a strong economic justification. In start-up companies, the need for financing is usually sufficient to provide a strong financial reason for a share issue.

For example, the company’s share capital consists of 100 000 shares. The company needs additional capital of €100 000 and in return for the investment a 20% stake in the company is given.

= 100 000 / (1-20%) = 125 000 shares

The share issue will therefore consist of 25 000 shares for an investment of EUR 100 000, giving the original owners 80% of the company.

The decision to issue shares is taken by the General Meeting, but can also be taken by unanimous vote of all shareholders.

However, simply deciding to issue shares will not save equity. The subscribers must obtain a subscription undertaking and payment for the share issue into the company’s account.

Convertible loan

A convertible loan is a loan in which the lender may receive, in addition to interest, the right to subscribe for shares in the debtor company at a pre-agreed price. The terms of a convertible loan may be capital loan or normal debt. In other words, an capital loan means a subordinated loan with terms and conditions.

When the loan is issued, the interest rate and the conversion rate are determined to determine the exchange ratio if the loan is converted into shares of the company.

The convertible loan is decided by the shareholders meeting or by the board of directors as authorised by the shareholders meeting. A resolution may also be adopted by a unanimous decision of the shareholders.

Are the revenue correctly recognized?

If your company sells long-term licences (SAAS = software as a service), a typical mistake is that the sales are not correctly recognized “revenue recognition”. I’ve seen a few times that a startup’s nice-looking revenue trajectory over a few financial years collapses when revenue recognition is corrected.

Suppose you sell a licence to a customer in December 202x for €1200 at 0% VAT for the period 1.12.202x – 30.11.202x. The accounting period is a calendar year. If the accounting is done incorrectly, the sale is recorded in full for December 202x, in which case the licence sale is recorded in full as revenue for the financial year 202x.

The correct way to record this sale is to periodise the sale, so that in the period 12/202x – 11/202x, each month 100 euros of turnover is recorded in the profit and loss account.

I illustrate the records with the figures above. In the upper example, no periodisation is applied, so that the turnover is fully recognised in the 202x financial year. In the lower example, sales are periodised, so that the turnover is recognised monthly.

Amortisation of Business Finland project income and expenses in the financial statements

Recognition of Business Finland Tempo grants in financial statements

Business Finland’s Tempo projects are non-repayable grants. The maximum grant amount is EUR 60 000 and is entered in the profit and loss account under other operating income.

Capitalisation restrictions for subsidised development costs

Costs covered by the subsidy must not be capitalised as development expenditure! For example, a company has incurred development costs of EUR 100 000 in the 202x financial year and has received a grant of EUR 50 000 from Business Finland to cover the above-mentioned development costs. The company can therefore capitalise a maximum of EUR 50 000 in development costs for the financial year.

Handling ongoing projects at financial year-end

If a Business Finland project is in progress at the turn of the financial year, the amount of project costs incurred by the balance sheet date should be determined. For example, the company has received a positive funding decision from Business Finland for a Tempo project. The financial year is the calendar year. The duration of the project is 1.11.20xx – 31.3.20xx. Business Finland pays the company an advance of EUR 35 000 in November 20xx.

Example: allocation of grant income based on realised costs

The project has a budget of €75 000, of which €50 000 is subsidised and €25 000 is self-financed by the company. Expenditure of EUR 25 000 has been incurred in the financial year 20xx, in which case the full amount of the EUR 35 000 grant cannot be recognised in the profit and loss account.

The correct proportion is to calculate the share of actual expenditure in the total budget, i.e. 25 000 / €75 000 = 33.3%. The amount of the project grant is EUR 50 000, of which 33.3% = EUR 16 650 can be allocated to other operating income for the financial year 2020. The remainder of the advance from Business Finland (EUR 35 000 – 16 650 = EUR 33 350) is recognised as a liability in the balance sheet.

Project tracking and accounting practices

Business Finland projects also require project monitoring. Check with your accountant that the costs allocated to the project have been allocated in the accounts to an accounting object, cost centre or dimension (all terms mean the same thing).

Do you need an accountancy firm that can advise you on the issues mentioned in this article? Valjas is a start-up’s best friend – so don’t hesitate to contact us!

Valjas helps with company finances

At Valjas, we help startups build a strong financial foundation from day one. Our team understands the unique challenges of early-stage growth — from managing Business Finland projects and funding reports to keeping accounting clear, compliant, and future-proof. We guide you through financial planning, cost tracking, and reporting so you can focus on scaling your business with confidence. With Valjas as your accounting partner, you gain more than bookkeeping — you gain a team that understands innovation, growth, and the numbers behind success.

We are not like other “accounting firms” but a clear, proactive partner.