Working capital is the money a company needs to keep everyday operations running. A simple example makes this clear. If you invoice customers at the end of the month with a 14-day payment term, you receive the money halfway through the next month. However, you still pay your employees at the end of the month. Because salaries go out before customer payments come in, you need working capital to cover that gap.

Some industries even operate with negative working capital, meaning very little money gets tied up in the business. Restaurants are a good example. Customers pay immediately by card or cash, while salaries and supplier invoices are paid later. Cash flows in quickly but flows out slowly, which keeps the need for working capital low.

For professional service firms, personnel costs dominate. Salaries and fringe benefits are usually the largest expense, followed by office rent unless work is done at client sites or from home. Payroll due dates are fixed and can’t be negotiated, but you can choose the actual payday. Office rent is typically paid at the beginning of each month.

That is why optimising working capital in professional services mainly comes down to two things: the timing of paydays and the timing of sales invoicing. Other expenses tend to be relatively small. Even if suppliers offer long payment terms, these usually don’t have a major impact on the total working capital needed.

1. Payday

Under no circumstances should you pay your wages for the current month! You can influence the payday and thus also the date on which your salary is paid. You need working capital because you pay employees’ salaries before you receive payment from customers for the sales invoices you send.

Always set the payday in the middle of the month following the month of earning. For example, the 10th or 15th. So, for example, your August salary will be paid on 15 September. In this case, the withholding tax and the health insurance contribution due on the salary will be due on 12 October in the above example.

If the payday is always the last day of the month, i.e. 31 August in the example, then withholding tax and health insurance contributions are due on 12 September. Compared to the example above, you pay these to the tax authorities one month earlier.

In principle, the payday is freely negotiable. Collective agreements may contain provisions on the payday, but these are usually negotiable. For hourly-paid workers, labour law requires that wages be paid twice a month. This should not be formally agreed otherwise, but it is quite common for hourly wages to be paid once a month. More on pay in our New employer guide.

Get your payday right from the start of your business. If you mess this up, changing your payday later will be a challenge. Employees have tuned their personal finances to payday and a change will cause an adjustment.

2. Sales invoicing

Always bill in advance if possible. For example, in project business, send an invoice for 20-30% of the total project amount at the beginning of the project. Invoice 2-3 instalments during the project and the last instalment as small as possible at the end of the project. Sometimes you hear stories from clients that they sold the project and invoiced after the project was completed. Then the customer complains and doesn’t pay the invoice at all. Such situations are effectively avoided by invoicing during the project.

You can also be billed in advance for hourly charges. For example, if the customer commits to buying at least a certain number of hours each month. Why should you be charged afterwards? The invoice can be balanced with the next month’s invoice if fewer or more hours were taken. Negotiate with the client and be bold in suggesting different types of billing models that will get the money back more quickly.

Do not give the customer long payment terms. In professional services, 14 days net is the most typical payment term. If you have to offer a longer payment term and need to raise working capital finance for it, please factor the longer payment term into your pricing.

Sometimes a long payment term to the customer can be a competitive advantage, but you also have to charge more for it. So take a longer payment term into account when pricing.

Monitor your trade receivables and send a first reminder 7pv after the due date. Move the invoice to collection 14 days after sending the reminder. Telephone collection, i.e. calling the customer about an outstanding invoice, is usually effective. However, always send a reminder in writing as well, so that it is remembered. For business customers, it is not necessary to send two payment reminders. You can also outsource the management of your receivables to a debt collection agency, which will monitor them on your behalf.

3. Optimising working capital through financing

Bank account limit

An overdraft is a good form of financing if your working capital needs fluctuate within a month. For example, on payday, a limit is needed and then, after a couple of weeks, the customer’s payments accumulate into cash inflows, so that the limit goes to zero.

An account limit means that your bank account can go into deficit within the agreed limit. For example, you can get a limit of €100 000 from your bank. The bank will charge the agreed commission on the amount of the limit, even if the limit is not used at all. The amount of the commission roughly starts from ~1% upwards. In addition, interest is paid to the bank on the use of the limit. The credit rating of the company has a significant impact on the bank’s pricing, i.e. how much commission and interest the bank charges.

Factoring

Factoring is the process of borrowing against trade receivables, i.e. invoice financing. Trade receivables serve as collateral for the loan. Usually the financing rate is between 70% and 80% of the invoice balance. Factoring is suitable for one-off or ongoing invoicing.

You send an invoice for €1000 to a customer. The invoice is sent to the factoring company, which adds its own transfer clause to the invoice, stating that the receivable has been transferred to the factoring company and the customer must pay it there. They then send the invoice to the final customer. The factoring company will immediately pay your company 70-80% of the invoice balance and deduct its own commission from the invoice. The rest is paid when the customer has paid the invoice to the factoring company. This gives you working capital, without waiting.

If the end-customer does not pay the invoice to the factoring company, you pay the loan back to the financier yourself. To get financing for an invoice, the customer must be creditworthy.

The price of a factoring service depends on the payment terms of the invoice. The longer the payment term, the higher the commission. Annual interest rates in factoring usually start from around 10% up to 30%. The annual interest rate refers to the cost of money, for example if you get a loan from a bank at 4% interest, it is proportional to the above. Factoring services offered by banks are usually the cheapest in terms of commission. However, banks’ systems and reports have not kept pace with other players, which is reflected in the availability of the service. Factoring is therefore not the cheapest form of financing. If you can cover your financing needs with other financing options, use them first.

Bank loan

A loan from a bank is also a good way to finance working capital needs. For business loans, the loan terms are shorter, typically around five years. You can negotiate a repayment grace period of, for example, six months at the beginning. After that, you repay the loan to the bank in instalments. Business loans are typically repayable on a flat-rate basis, meaning that the amount of the repayment remains the same throughout. The interest rate varies from repayment to repayment; if the interest rate stays the same, the interest rate decreases each month as the principal of the loan decreases.

Sale of trade receivables

The difference with factoring is that the credit risk is transferred. This means that the party buying the invoice bears the credit risk on the receivable. So if you sell the invoice, you outsource the rickshaw of invoicing. This is why receivables from customers with a poor credit rating are not purchased. You will receive an immediate settlement of the entire invoice, with the accountant retaining his own commission. The amount of the commission depends on the payment term, with short payment terms being the cheapest and longer terms the most expensive. In any case, this is a more expensive option than factoring, albeit more flexible.

If the customer complains about an invoice you have sold, you will have to reclaim the claim from the finance company.

4. Tip on VAT

If you invoice for work done at the end of each month, the invoice will be issued on the first day of the following month. This way, you postpone the payment of VAT for a month. Ask your accountant to periodise the invoice in the accounts for the month to which it relates.

If you invoice hourly in arrears, set the invoicing period at half a month. In other words, invoice on the 15th for work done at the beginning of the month. At the end of the month, the latter, taking into account the above-mentioned invoice dating. In other words, the invoice for work done between the 16th and the 31st is dated the first day of the following month. The accrual is made without VAT. For more information on “alv’s” , see the Tax Office website.

Working capital commitment calculations

The fictitious specialist company employs 10 people. Customers are expected to pay their invoices on the due date. In real life, of course, this is not always the case. The example is also simplified for VAT purposes, as the purchases in this example do not include deductible VAT. For example, optimise your working capital as follows.

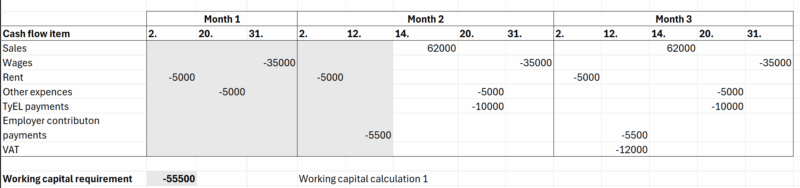

Calculation 1

- Sales invoices are always issued at the end of the month with a 14-day payment term.

- Employees’ payday is the last day of the month.

- The gross salaries of the employees total EUR 40 000.

- TyEL contribution on wages EUR 10 000.

- The withholding tax on wages and salaries is €5,000 and the sickness insurance contribution is €500, making a total of €5,500.

- Other expenses 5000 euros, payable monthly on the 20th.

The working capital requirement is EUR 55 500. The company pays rent twice, other expenses, salaries and withholding tax on wages before it receives payment from its customers for sales invoices.

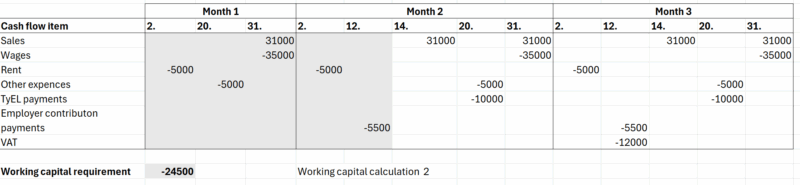

Calculation 2

- Sales invoices are issued twice a month, on the 15th and at the end of the month, with a payment term of 14 days.

- Otherwise, the same figures as in the first calculation.

The calculation assumes that customers pay the invoices sent on the 15th so that the company receives payments from customers for the payment of wages. The working capital requirement is reduced to EUR 24 500.

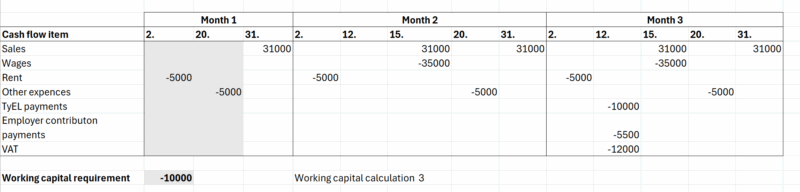

Calculation 3

- The company’s payday is the 15th of the following month.

- Billing will be done twice a month, otherwise as in calculation one.

The working capital requirement is reduced to EUR 10 000, as the payday is the following month and customers are paid before they are paid.

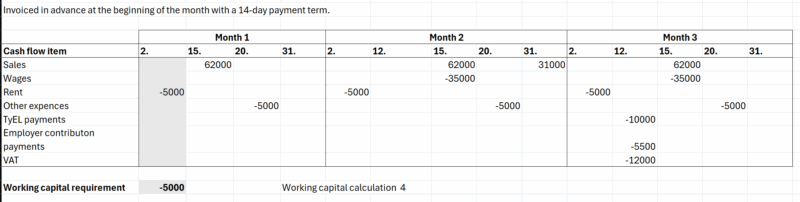

Calculation 4

- Invoiced in advance at the beginning of the month with a 14-day payment term.

The working capital requirement is reduced to €5,000.

As you can see from the examples above, the billing interval and payday setting have a significant impact on working capital needs.

If you want to take the guesswork out of working capital and make your cash flow feel predictable, our team is here to help. At Valjas, we combine smart tools with real human expertise to keep your numbers moving in the right direction.

Let’s make your finances work for you, not the other way around.